We recently wrote a piece in Crunchbase: https://news.crunchbase.com/news/vc-investments-startups-unicorns/

The pace of dealmaking is frenzied: The 61 percent year-over-year increase in funding for the first half of 2021 is a staggering leap, and the 136 new unicorns in the second quarter of this year are rightly raising eyebrows since the entirety of 2020 produced a mere 128.

It’s reasonable to expect some form of correction, but anything parallel to the 2000 crash is most likely overstated.

Here’s why.

First, we’ve become conditioned to these cycles in venture capital. The recovery from 2000 was slow and painful, but if we look back to 2008 and its subsequent recovery years, VCs increasingly seized the correction as a buying opportunity and nurtured startups like Slack, Airbnb and Dropbox.

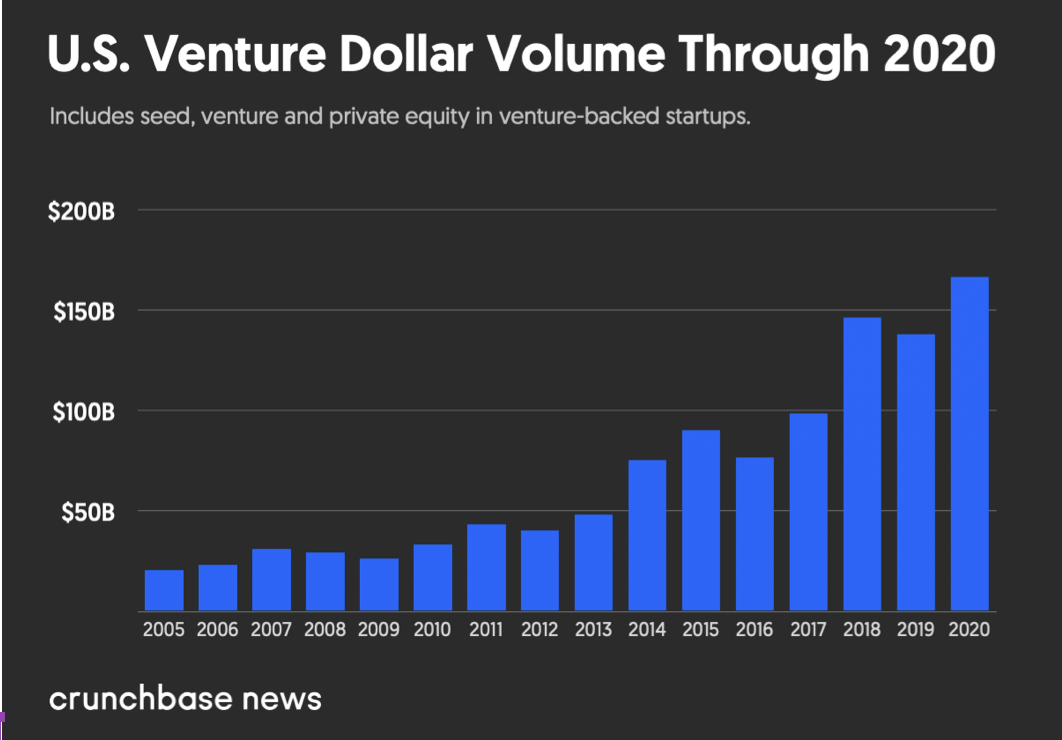

The slowdown in investment lasted just three years and was far less marked than after the turn of the millennium, demonstrating much stronger conviction among VCs in the long-term potential of tech startup investments.

Next, investors are desperate for returns. A major component of the current pace of dealmaking in venture is simply a matter of getting massive inflows of LP money out the door. Other investments have become far less enticing as returns have become more muted, so even when some of these investments that have been made far too quickly blow up, capital will keep piling into the sector.

Perhaps the biggest buoying factor in this current market, though, is monetary policy both in the U.S. and abroad. The capital unleashed by the Federal Reserve and European Central Bank during this pandemic, in particular, has greased the wheels of the venture investing machine beyond comparison.

Like it or not, the trillions of dollars pumped into the economy by the Fed over the last year has made the wealthiest Americans (read: LPs) much richer during the pandemic, and they’ve dumped record volumes of that capital back into VC. So as long as the Fed continues to take this track when faced with economic downturns, VCs will continue to reap benefits for taking on that additional risk.

All of this adds up to increasingly flattened recovery curves for the venture industry. Not only are investors less inclined to spooking, but with an accommodative government, any hit they face may be quickly wiped away, freeing them to continue chasing after the high returns that investing in high-growth startups can provide.

Certainly, slapdash dealmaking done without proper due diligence will come back to bite plenty of VC firms, but don’t be expecting another 2000-style crash with a prolonged recovery when the music stops this time around.

It will just reset the stopwatch, and VCs will be lining back up for the next sprint in short order, cognizant that the winners of this next race will land stakes in the next Uber or Shopify.